Business Structure 101: Proprietorship vs LLP vs Private Limited Company — Which One Should You Choose?

Starting a business comes with one unavoidable early decision: choosing the right business structure in India.

Most first-time founders either rush past this question (“I’ll sort it out later”) or get paralysed by it, convinced that picking the “wrong” structure will doom the business. Neither approach is right.

The truth is more practical: your business structure is a starting point, not a permanent identity. The right choice depends on where you are today — your team size, your goals, your risk appetite, and whether you need to raise funding in the near future.

This guide breaks down the three most realistic options for new businesses in India — Sole Proprietorship, LLP (Limited Liability Partnership), and Private Limited Company — in plain language, with no legal jargon. By the end, you’ll know exactly which one makes sense for your situation.

What Is a Business Structure — and Why Does It Matter?

A business structure (also called a “legal entity type”) is the formal shape your business takes in the eyes of the law. It determines:

- Who is legally responsible if the business has debts or legal disputes

- How your business is taxed and how profits are reported

- What documents and compliance you’re required to maintain

- How much credibility your business signals to banks, partners, and platforms

- Whether you can raise investment from external investors in the future

Every downstream decision — opening a bank account, registering for GST, listing on Amazon, applying for a business loan — connects back to your business structure. Getting this right at the start saves significant time and paperwork later.

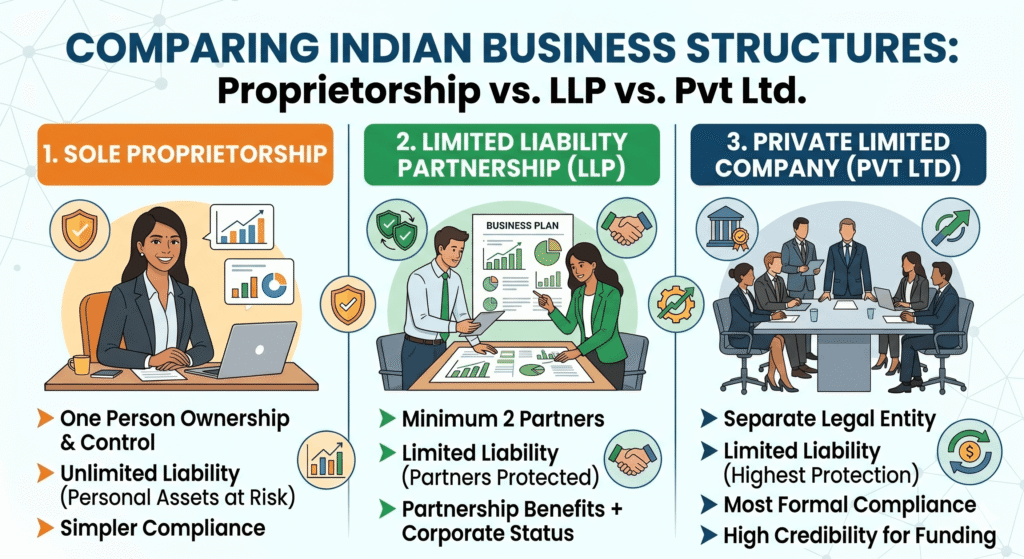

The Three Main Options for New Indian Businesses

Before comparing them, here’s a quick summary:

| Structure | Legal Liability | Compliance | Setup Cost | Best For |

|---|---|---|---|---|

| Sole Proprietorship | Unlimited (you = business) | Minimal | Near zero | Solo founders starting out |

| LLP | Limited (partners protected) | Moderate | ₹5,000–₹15,000 | Co-founders, professionals |

| Private Limited Company | Limited (company is separate) | High | ₹10,000–₹25,000+ | Scale-focused, investment-seeking |

Now let’s go deep on each.

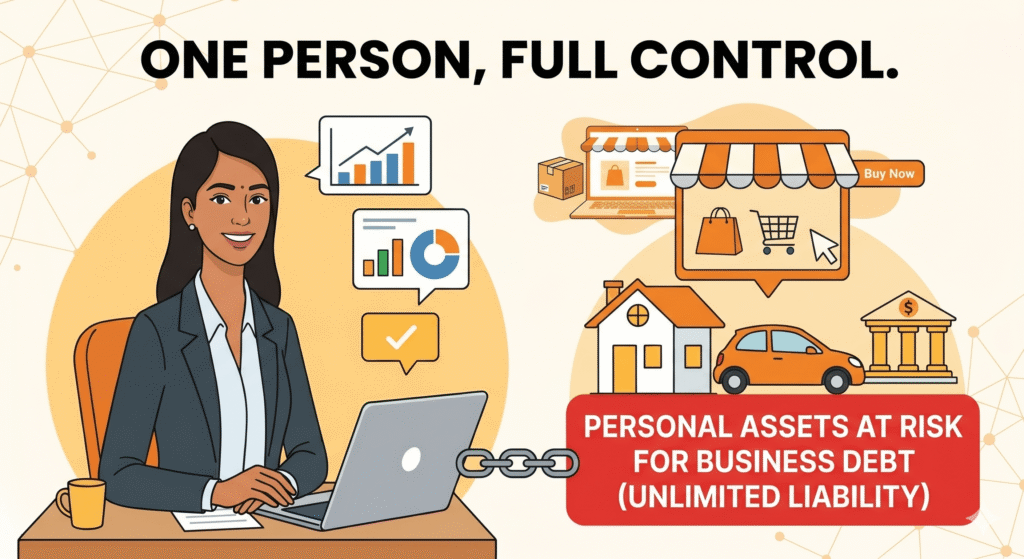

Option 1: Sole Proprietorship

What It Is

A sole proprietorship is the simplest business form in India. There is no legal separation between you and your business — legally, you are the business. Your personal PAN becomes your business PAN. Your personal bank account (or a current account opened in your name) is your business account.

There is no formal government registration specifically for a “proprietorship” — it is established by simply starting operations and obtaining the necessary licenses for your activity (such as GST registration, FSSAI, MSME/Udyam, etc.).

Who It Is For

Sole proprietorship is the default starting point for the majority of first-time entrepreneurs in India, particularly:

- Solo founders who are testing a product or business idea before committing to a formal structure

- Ecommerce sellers starting on Amazon, Flipkart, or Meesho

- Freelancers, consultants, and service providers

- Artisans, home-based makers, and regional product sellers

Advantages

Speed and simplicity. You can begin operating almost immediately. There’s no registration process, no minimum capital requirement, and no requirement to file separate business accounts.

Zero direct setup cost. The only costs are the licenses and registrations your specific business requires (GST, FSSAI, etc.) — not a structure registration fee.

Minimal compliance. No separate business tax returns — your business income is reported in your personal Income Tax return under “profits and gains from business or profession.”

Full control. All decisions are yours. No partners, no board, no shareholder approvals.

Exact Tax Rates for Proprietorships (FY 2026-27)

A proprietorship isn’t taxed separately — your business profit is simply added to your personal income and taxed at individual slab rates. Under the default New Tax Regime (Section 115BAC), here’s where you stand:

- If your total taxable income (business profit + any other income) is up to ₹12,00,000, you pay zero tax — thanks to the full rebate under Section 87A.

- For salaried individuals also running a proprietorship, the tax-free threshold extends to ₹12,75,000 after the standard deduction.

- Beyond the rebate threshold, rates are progressive, reaching the highest slab of 30% plus a 4% Health and Education Cess on higher income.

- Surcharges apply progressively once income crosses ₹50 lakh, pushing the effective top rate to roughly 31.2% at higher income levels.

What this means practically: if you’re a new seller and your net profit for the year stays under ₹12 lakh, you may end up paying nothing in income tax on your business income at all. This is one of the most underrated advantages of starting as a proprietorship — it’s not just simple, it’s genuinely tax-efficient at the income levels most new sellers operate at in year one.

Disadvantages

Unlimited liability. This is the most important limitation to understand. If your business takes on a debt it cannot repay, or faces a legal claim, your personal assets — savings, property — are at risk. You and the business are legally the same entity.

Limited credibility for large contracts. Some larger buyers, platform partners, and institutional vendors prefer dealing with registered legal entities (LLP or Pvt Ltd), particularly for high-value contracts or credit arrangements.

No separate legal identity. The business cannot own assets, enter contracts, or hold intellectual property in its own name — it all flows through you personally.

Harder to bring in co-founders or investors. A proprietorship cannot have partners or shareholders by definition. If you want to bring in a co-founder later, you’ll need to convert to a different structure.

Is a Proprietorship “Upgradeable”?

Yes. Many successful Indian D2C brands — including several that now operate as Private Limited companies — began as proprietorships. You can convert a proprietorship to an LLP or Private Limited Company as your business grows, transfers assets, and needs to scale. It involves some paperwork and costs, but is entirely standard and well-understood by CAs in India.

Bottom line on proprietorship: If you’re starting solo, testing a product, or just getting your first few sales on a marketplace — start here. Get your GST, open your business current account, start building revenue, and convert when the business needs it.

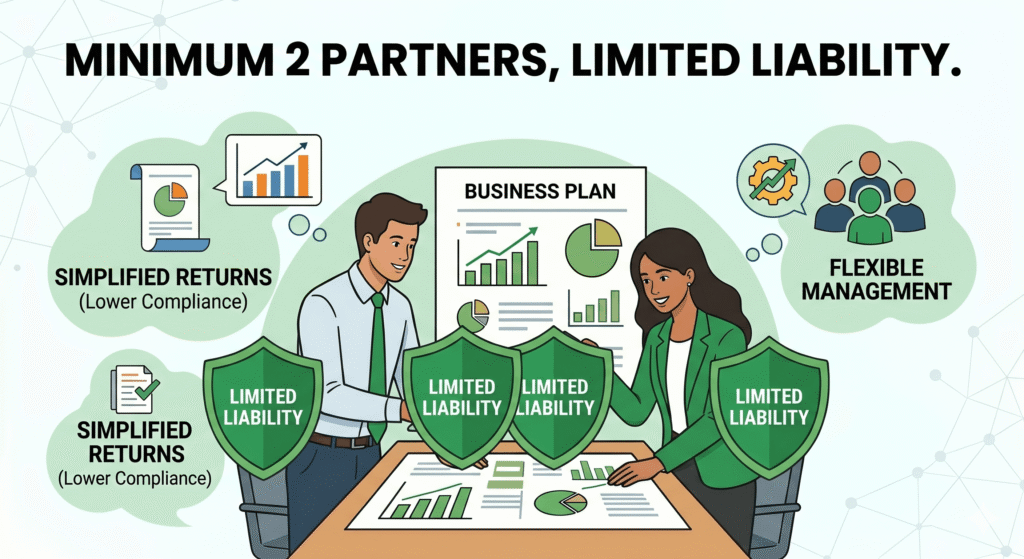

Option 2: LLP (Limited Liability Partnership)

What It Is

An LLP is a formal legal entity registered with the Ministry of Corporate Affairs (MCA). It combines the flexibility of a traditional partnership (shared ownership, easier management) with “limited liability” — meaning the partners’ personal assets are protected if the business faces claims, as long as the partners acted within the law.

An LLP requires a minimum of two designated partners, both of whom must have a Director Identification Number (DIN) and a Digital Signature Certificate (DSC). It is registered through the MCA portal and gets a unique LLP Identification Number (LLPIN).

Who It Is For

LLP works well for:

- Co-founders starting a business together who want formal shared ownership with legal protection

- Professional services firms (CA firms, law firms, design studios, consulting practices) — the LLP structure was specifically designed with these in mind

- Businesses that want limited liability without the full compliance burden of a Pvt Ltd

Advantages

Limited liability. Partners are not personally liable for the LLP’s debts beyond their agreed contribution — personal assets are protected.

Formal co-ownership structure. An LLP agreement defines each partner’s rights, responsibilities, and profit-sharing — far cleaner than informal verbal arrangements.

Lower compliance than Pvt Ltd. LLPs don’t need board meetings, have simpler annual compliance requirements, and generally have lower ongoing costs than Pvt Ltd companies.

Audit threshold. LLPs whose turnover is below ₹40 lakhs and contribution is below ₹25 lakhs are exempt from mandatory audit — reducing compliance costs for smaller operations.

Tax efficiency. LLPs are taxed as a firm, with no dividend distribution tax — partners receive their share of profits without it being taxed again at their hands.

Exact Tax Rates for LLPs (FY 2026-27)

Unlike a proprietorship, an LLP is taxed as a separate entity, and the rates are flat rather than slab-based:

- LLPs pay a flat 30% tax on total taxable income — there is no rebate or lower slab, regardless of how small the profit is.

- A 12% surcharge applies if total income exceeds ₹1 crore, plus the standard 4% Health and Education Cess on top of tax + surcharge.

- This works out to an effective rate of 31.2% for income up to ₹1 crore, and 34.944% for income above ₹1 crore.

- If your normal tax liability comes out lower than 18.5% of adjusted total income, the Alternate Minimum Tax (AMT) under Section 115JC kicks in at 18.5% instead.

- Once tax is paid at the entity level, any profit share distributed to partners is completely tax-exempt in the partners’ hands under Section 10(2A) — no double taxation on withdrawal.

Two rules that matter if you’re a working partner:

- Section 194T: If the LLP pays a partner remuneration, salary, interest, bonus, or commission exceeding ₹20,000 in a financial year, the LLP must deduct 10% TDS on that payout.

- Section 40(b): Working partners can deduct their remuneration from the LLP’s taxable income, but only up to statutory limits set by law (and interest paid on partner capital is deductible only up to 12% per annum). This remuneration deduction is what makes LLPs tax-efficient in practice — it shifts some profit out of the flat 30% entity-level tax and into the partner’s personal return instead.

Practical takeaway: an LLP only starts looking more tax-efficient than a proprietorship once profits comfortably exceed the ₹12 lakh personal-rebate threshold — below that, the proprietorship’s 0% rate (via Section 87A) is hard to beat.

Disadvantages

Minimum two partners required. A solo founder cannot form an LLP.

No equity-based fundraising. LLPs cannot issue shares or raise equity investment from angel investors or VCs. This is a significant limitation if you plan to raise external funding.

Less “prestigious” than Pvt Ltd for certain purposes. Some larger companies and investors in India still view Pvt Ltd as the more credible structure for scaling businesses, particularly in B2B contexts.

Winding up is more complex. Closing an LLP is procedurally more involved than simply stopping operations as a proprietor.

Bottom line on LLP: If you’re starting with one or more co-founders, want legal protection without the full overhead of a Pvt Ltd, and don’t expect to raise equity investment in the near term — LLP is a strong choice.

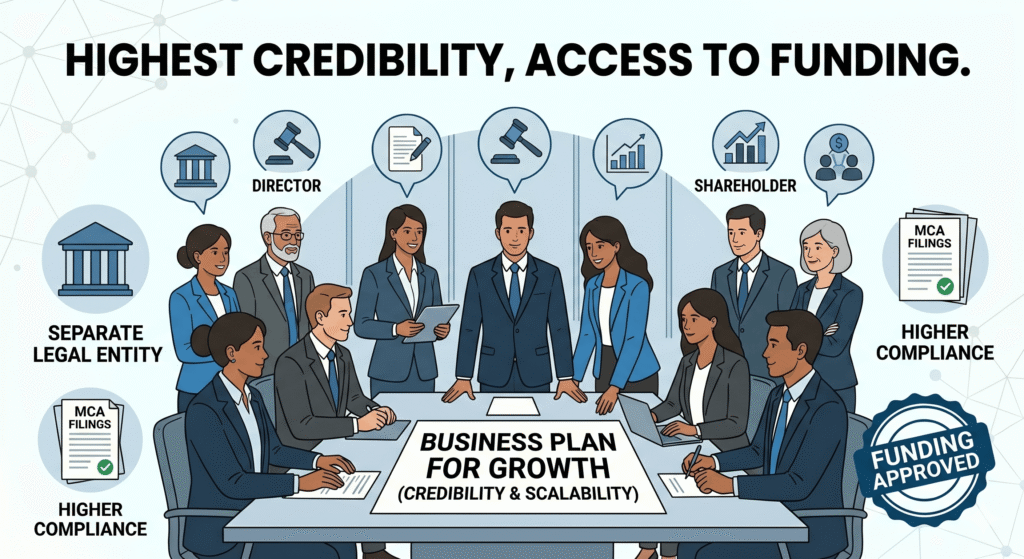

Option 3: Private Limited Company (Pvt Ltd)

What It Is

A Private Limited Company is the most formally structured option, and the one most investors, large partners, and funding platforms expect. It is a separate legal entity — it exists independently of its founders, can own assets, enter contracts, and be held liable in its own name.

A Pvt Ltd is registered with the MCA and requires:

- Minimum two directors (and up to fifteen)

- Minimum two shareholders (can be the same as directors)

- A Memorandum of Association (MoA) and Articles of Association (AoA)

- A registered office address

- Director Identification Numbers (DIN) and Digital Signature Certificates (DSC) for all directors

- A minimum authorised share capital (the law requires at least ₹1 lakh, though no minimum paid-up capital is mandatory post-2015)

Who It Is For

Pvt Ltd is the right choice for:

- Founders who are confident about scaling and plan to raise investment from angels, VCs, or institutional sources

- Businesses building a team and needing to offer ESOPs (employee stock options)

- Brands targeting large institutional buyers or B2B clients who require working with a registered company

- Founders building for acquisition or long-term brand exit

Advantages

Separate legal entity. The company can own property, sign contracts, and take on liability — completely separate from the founders.

Limited liability. Shareholders’ personal assets are protected. Founders’ liability is limited to their shareholding in the company.

Equity fundraising. Pvt Ltd companies can issue shares to investors — essential for angel or VC funding.

Highest credibility. For most institutional buyers, large platforms, and serious B2B partnerships, a Pvt Ltd signals permanence, governance, and accountability.

ESOPs and team incentives. Can structure employee stock option plans to attract and retain talent.

Brand registry advantages. Platforms like Amazon Brand Registry and Shopify Partner programs often work more smoothly with entities that have formalized IP ownership — easier to demonstrate as a Pvt Ltd.

Exact Tax Rates for Private Limited Companies (FY 2026-27)

Pvt Ltd companies have more tax regime choices than proprietorships or LLPs — and picking the right one matters:

Concessional Regime — Section 115BAA: A company can opt for a flat 22% base tax rate. After adding the mandatory 10% surcharge and 4% cess, the effective rate is 25.168%. Companies under this regime are completely exempt from Minimum Alternate Tax (MAT) — a meaningful simplification. The trade-off: opting in is irrevocable, and you give up most deductions under Chapter VI-A and other standard exemptions.

Normal Regime (turnover-based): If you don’t opt into 115BAA, the base rate is 25% for companies with turnover up to ₹400 crore in the preceding year (30% above that). A 7% surcharge applies on income between ₹1 crore–₹10 crore, and 12% above ₹10 crore. Under this regime, MAT applies at 15% of book profits (Section 115JB), with unused MAT credit carryable forward for up to 15 years.

Section 115BAB (Manufacturing): Offers a highly concessional 15% rate (effective ~17.16%) — but this is restricted to companies incorporated after October 1, 2019 that began manufacturing by March 31, 2024, so it’s not available for new setups today.

Two incentives worth knowing about if you’re building to scale:

- Section 80-IAC Tax Holiday: DPIIT-recognised startups (Pvt Ltd or LLP) can claim a 100% profit deduction for any 3 consecutive years within their first 10 years — provided turnover stays under ₹100 crore and incorporation happens before March 31, 2030. Note: this cannot be combined with the Section 115BAA concessional rate — you choose one or the other.

- Angel Tax Abolished: Since April 1, 2025, Section 56(2)(viib) has been repealed — share premium raised from domestic or foreign investors is no longer taxed. This removed a major friction point for equity-funded startups raising at a premium valuation.

Practical takeaway: for most new Pvt Ltd companies that aren’t immediately profitable or aren’t claiming heavy deductions, Section 115BAA’s 25.168% flat rate is usually the simplest and most predictable choice — and it removes MAT from your compliance checklist entirely.

Disadvantages

Highest compliance burden. Pvt Ltd companies must hold Annual General Meetings (AGMs), file annual returns with the MCA and Registrar of Companies (RoC), maintain statutory registers, and comply with Companies Act 2013 requirements throughout the year. This usually means paying a CA for ongoing compliance.

Higher setup and maintenance cost. Setup involves professional fees (₹10,000–₹25,000+ typically), and annual compliance costs (ROC filings, audit, etc.) can run ₹15,000–₹50,000+ per year depending on your CA.

More complex to wind up. Striking off a Pvt Ltd company is a formal legal process that takes time and documentation.

Minimum two directors/shareholders. Solo founders either need to bring in a co-founder or add a nominee director (a common practice).

Worth knowing if you’re building for scale: DPIIT-recognised startups can claim a 100% tax holiday on profits for any 3 consecutive years in their first 10 years (Section 80-IAC), and since April 2025, angel tax on investor share premium has been fully abolished (Section 56(2)(viib) repealed) — removing a major historical friction point for equity fundraising in India.

Bottom line on Pvt Ltd: If you’re building to scale, plan to raise investment, or are targeting large institutional partnerships — go Pvt Ltd from the start. If you’re in early testing mode, the compliance overhead is likely unnecessary friction until you have product-market fit.

How to Choose: A Simple Decision Framework

Ask yourself these four questions:

1. Am I starting solo or with a co-founder?

- Solo → Proprietorship (or Pvt Ltd with a nominee director if scale is the plan)

- With co-founder → LLP or Pvt Ltd

2. Do I plan to raise external investment (angel/VC) in the next 12–24 months?

- Yes → Pvt Ltd (only structure that allows equity fundraising)

- No → Proprietorship or LLP

3. Am I still testing the product, or do I have validated demand?

- Testing → Proprietorship (lowest cost and friction to start)

- Validated demand, ready to scale → LLP or Pvt Ltd

4. Is my compliance budget limited right now?

- Yes → Proprietorship or LLP

- No → Pvt Ltd

The Most Common Path for New Ecommerce Founders

The most common — and typically the most practical — path for first-time physical product sellers in India:

Start as a Sole Proprietorship → get GST and Udyam registration → build initial revenue → convert to Pvt Ltd when scale or investment requires it.

This is not “cutting corners.” It’s sequencing correctly. A proprietorship with valid GST, a proper current account, and a trademark-filed brand name is a fully legitimate, operating business — and is exactly how thousands of successful D2C brands in India began.

What About Registration — Do You Need to “Register” a Proprietorship?

One of the most common misconceptions is that a proprietorship requires a specific registration. It does not. What you need are the licenses and registrations that apply to your business activity:

- GST Registration — mandatory for any marketplace seller, regardless of turnover (read our complete GST registration guide for ecommerce sellers)

- Udyam/MSME Registration — free, online, and takes minutes (read our Udyam registration guide)

- Trademark Registration — protects your brand name and logo (read our trademark guide for new brands)

- Current Bank Account — open in your name/trade name, using your PAN and GST as primary documents

- FSSAI (if applicable) — for food and beverage products

These registrations collectively establish your business identity, even without a formal “proprietorship registration.”

Converting From One Structure to Another — The Actual Process

Conversion is normal, not a failure — most scaling D2C brands in India go through exactly this path. But it’s worth knowing that Indian law doesn’t allow a simple “rename” between structures. Each route has its own statutory process. Here’s what’s actually involved.

Proprietorship → LLP

Because a proprietorship isn’t a separate legal entity, you can’t directly “convert” it — instead, you incorporate a fresh LLP and transfer the business into it.

- Incorporate the new LLP. You’ll need at least one more partner (LLPs require minimum two). Obtain Digital Signature Certificates (DSC) and DPINs, reserve a name via the RUN-LLP service, and file the FiLLiP incorporation form on the MCA portal.

- Execute a Business Transfer Agreement (BTA). This document formally transfers all assets, liabilities, and contracts from you (the proprietor) to the new LLP — typically at book value, to keep the transfer tax-neutral.

- Transfer your Input Tax Credit via Form GST ITC-02. Your old GSTIN can’t simply be renamed (it’s tied to your personal PAN); the LLP needs its own fresh GSTIN. To move any unused ITC across, file Form GST ITC-02 on the GST portal, supported by a CA certificate confirming the transfer includes provision for liabilities. Done correctly as a “going concern” transfer, this is exempt from GST.

Proprietorship → Private Limited Company

This is the most common upgrade path for ecommerce founders planning to scale or raise funding.

The tax-neutral route — Section 47(xiv): To avoid the transfer triggering capital gains tax, three conditions must all be met:

- All assets and liabilities of the proprietorship must become assets and liabilities of the new company.

- You (the original proprietor) must hold at least 50% of the voting power in the new company, and maintain it for a 5-year lock-in period.

- You must receive only shares as consideration for the transfer — no cash, no debt instruments.

If you break any of these conditions during the 5 years (for example, diluting below 50% to bring in investors early), the exemption is voided and the original transfer becomes taxable retroactively as capital gains in the year you broke the condition.

If you can’t meet those conditions (e.g., you need to dilute below 50% immediately to onboard a co-founder or investor), the transfer is instead structured as a slump sale under Section 50B — the entire business moves as a going concern for one lump-sum price. Capital gains here are calculated on “net worth” (book value of assets minus liabilities), taxed at a flat 20% long-term capital gains rate if you’ve held the business over 36 months.

Don’t forget your trademark. If you’ve registered a trademark as a proprietor, it needs to be formally reassigned to the new company via a Trademark Assignment Deed, with Form TM-P filed within 6 months of the transfer date.

Post-conversion filings: Form PAS-3 (share allotment), Form INC-20A (declaration of commencement of business, within 180 days), Form GST ITC-02 (credit transfer).

Important penalty to know: missing the 180-day window for Form INC-20A carries a ₹50,000 penalty for the company and ₹1,000 per day for each director (up to ₹10 lakh per director). The ROC can also strike off the company name if it stays inactive. Don’t let this filing slip.

LLP → Private Limited Company

Unlike a proprietorship, an LLP can convert directly into a Pvt Ltd through a statutory process (Section 366, Companies Act 2013) — all assets, contracts, licenses, and liabilities transfer automatically by operation of law, no separate BTA needed.

Key steps: unanimous written consent from all partners → a CA-certified statement of assets and liabilities (must be dated within 6 days of filing Form URC-1 — a strict timeline) → public notice in two newspapers (Form URC-2, one English + one vernacular) → a mandatory 21-day waiting period after publication for creditor objections → NOCs from secured creditors → filing Form URC-1 with the SPICe+ suite on the MCA portal.

Once approved, you get a fresh Certificate of Incorporation. Within 15 days, notify the Registrar of LLPs to formally close out the old LLP. You’ll need a new PAN and TAN for the company (these don’t carry over), and file Form INC-20A within 180 days — same ₹50,000+ penalty risk applies if missed.

Private Limited Company → LLP

Less common, but some founders move this direction when growth slows and the compliance overhead of a Pvt Ltd no longer makes sense. This is only tax-exempt under Section 47(xiiib) if all of these hold:

- The company’s turnover never exceeded ₹60 lakh in any of the preceding 3 financial years.

- The company’s total assets never exceeded ₹5 crore in any of the preceding 3 financial years.

- All shareholders become LLP partners in matching proportions, retaining at least 50% profit share for 5 years.

- No payouts from pre-conversion accumulated profits for 3 years after conversion.

Breaching any condition retroactively cancels the exemption — the gain becomes taxable to the LLP and partners in the year of breach.

The bottom line on all of this: conversion is well-trodden ground with clear statutory routes — but each path has hard deadlines (15 days, 21 days, 180 days, 6 days) and lock-in conditions (3-5 years) that, if missed or broken, can retroactively undo your tax-neutral treatment. This is exactly the kind of process where a CA earns their fee — don’t attempt a conversion without one.

Quick Comparison at a Glance

| Sole Proprietorship | LLP | Private Limited | |

|---|---|---|---|

| Minimum founders | 1 | 2 | 2 |

| Legal identity | No (you = business) | Yes (separate entity) | Yes (separate entity) |

| Personal liability | Unlimited | Limited | Limited |

| Setup cost | Near zero | ₹5,000–₹15,000 | ₹10,000–₹25,000+ |

| Annual compliance | Minimal (personal ITR) | Moderate | High |

| Equity fundraising | No | No | Yes |

| GST required (ecom) | Yes | Yes | Yes |

| Best first step for | Solo founders, early-stage | Co-founders, no investor plan | Scale-focused, investor-ready |

| Can upgrade to Pvt Ltd? | Yes | Yes | N/A |

Tax Comparison at a Glance (FY 2026-27)

Putting all the tax details from above side by side:

| Tax Parameter | Sole Proprietorship | LLP | Private Limited Company |

|---|---|---|---|

| Tax status | Taxed as individual personal income | Taxed as separate entity | Taxed as separate entity |

| Effective rate (income up to ₹1 Cr) | Progressive slabs, max ~31.2% | Flat 31.2% (incl. 4% cess) | 25.168% (Sec 115BAA) or ~26% (normal regime) |

| Effective rate (income above ₹1 Cr) | Progressive slabs + surcharge | Flat 34.944% (incl. 12% surcharge) | Base 22-30% + surcharge (7-12%) + 4% cess |

| Rebate / zero-tax threshold | Up to ₹12,00,000 (Sec 87A) | None | None |

| MAT/AMT | Not applicable | AMT at 18.5% (Sec 115JC) | 15% of book profits (waived under 115BAA) |

| Tax on profit withdrawal | Not applicable (it’s your income) | Exempt under Sec 10(2A) | Dividends taxed in shareholders’ hands |

| TDS on owner/partner payouts | Not applicable | 10% TDS under Sec 194T (above ₹20,000) | Standard salary/dividend TDS rules apply |

The simplest way to think about it: if your annual profit is realistically going to stay under ₹12 lakh in year one, a proprietorship is hard to beat on pure tax efficiency — you may pay nothing. Once profits grow past that and you need fundraising flexibility, the calculation shifts toward LLP or Pvt Ltd depending on your growth plans.

About This Article

This article is intended for general informational purposes and reflects the legal, regulatory, and tax environment in India for FY 2025-26 and FY 2026-27 as of early 2026. Business registration requirements, compliance obligations, tax rates, surcharge thresholds, and exemption conditions (including Sections 87A, 115BAA, 115BAB, 47(xiv), 47(xiiib), and 194T) are subject to change through the Union Budget and subsequent notifications. Always verify current rates on the Income Tax e-filing portal and consult a qualified Chartered Accountant (CA) or Company Secretary (CS) for advice specific to your situation before making structural or tax decisions.